Best and Cheapest Home Insurance Companies in Indiana for 2026

Allstate has the cheapest rates in Indiana for most people, at an average of $1,026/year. | ||

Home insurance in Indiana averages $2,639/year, which is 10% higher than the national average. | ||

People living in northeastern Indiana usually pay the cheapest rates, while southeastern Indiana homeowners have more expensive policies. |

Allstate has the cheapest rates in Indiana for most people, at an average of $1,026/year. | ||

Indiana home insurance costs $2,639/year, on average. But average rates can differ by up to $924, depending on where you live. |

Find Cheap Home Insurance Quotes in Indiana

Who has the best cheap home insurance in Indiana?

What company has the cheapest home insurance in Indiana?

Allstate has the cheapest home insurance rates in Indiana, no matter how much coverage you need.

Find Cheap Home Insurance Quotes in Indiana

- Allstate's average rates for Indiana home insurance are cheap no matter how much coverage you need for your house. For a house with $350,000 in dwelling coverage, Allstate's average rate is less than half of the state average.

- State Farm is also a consistently cheap option and a great choice if you want to bundle your home and auto insurance.

- If you own a new home, Allstate and Erie have the cheapest rates in Indiana. A policy with $350,000 in dwelling coverage costs an average of $612 per year from Allstate and $738 per year from Erie.

Best cheap IN home insurance by dwelling amount

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| Allstate | 4.0 out of 5 | $793 | |

| State Farm | 3.5 out of 5 | $1,132 | |

| Cincinnati | 3.3 out of 5 | $1,146 | |

| Farmers | 3.0 out of 5 | $1,517 | |

| Progressive | 3.5 out of 5 | $1,848 | |

| American Family | 2.5 out of 5 | $1,861 | |

| Farm Bureau | 0.8 out of 5 | $2,156 | |

| Nationwide | 2.5 out of 5 | $2,212 | |

| Erie | 2.5 out of 5 | $2,300 | |

| Auto-Owners | 3.0 out of 5 | $2,368 | |

| Grange | 2.0 out of 5 | $2,556 | |

| USAA* | 4.5 out of 5 | $1,300 | |

*USAA is only available to military members, veterans and some of their family members.

Key takeaways

- Indiana home insurance rates went up by about 4.4% in 2025, a bit less than the average hike of 5.6% nationally.

- State Farm's rates have stayed fairly steady, with basically no increase between 2024 and 2025.

- Auto-Owners had one of the biggest rate increases in Indiana, with rates going up about 12% between 2024 and 2025.

- Shopping around and comparing quotes can help you get the best deal. But remember to look at more than just price. Make sure a company has the coverage you need, and consider service and claims experience, too.

Best home insurance in Indiana for most people: Allstate

-

Annual cost$1,026Average rate for a $350,000 home

-

Monthly cost$86Average rate for a $350,000 home

-

AverageCustomer complaints

Best home insurance in Indiana for bundling: State Farm

-

Annual cost$1,513Average rate for a $350,000 home

-

Monthly cost$126Average rate for a $350,000 home

-

AverageCustomer complaints

Best home insurance in Indiana for customer service: Erie

-

Annual cost$3,585Average rate for a $350,000 home

-

Monthly cost$299Average rate for a $350,000 home

-

LowCustomer complaints

What are the top-rated home insurance companies in Indiana?

USAA and Allstate are the top-rated home insurance companies in Indiana.

Both companies earn high marks from ValuePenguin's insurance experts. USAA also earned better-than-average scores from J.D. Power for customer and claims satisfaction.

USAA has very few complaints about its home insurance, according to the National Association of Insurance Commissioners (NAIC). But remember, you can only get USAA if you're a veteran, military member or qualifying family member.

Company |

Rating

|

Complaints

|

|---|---|---|

| USAA | 4.5 out of 5 | Low |

| Allstate | 4.0 out of 5 | Average |

| Progressive | 3.5 out of 5 | Low |

| State Farm | 3.5 out of 5 | Average |

| Cincinnati | 3.3 out of 5 | Low |

| Auto-Owners | 3.0 out of 5 | Low |

| Farmers | 3.0 out of 5 | Average |

| American Family | 2.5 out of 5 | Average |

| Erie | 2.5 out of 5 | Low |

| Nationwide | 2.5 out of 5 | High |

| Grange | 2.0 out of 5 | High |

| Farm Bureau | 0.8 out of 5 | High |

What's the average home insurance cost in Indiana?

Homeowners insurance in Indiana costs an average of $2,639 per year for $350,000 in dwelling coverage.

That's about 10% higher than the national average of $2,395 per year for $350,000 in dwelling coverage.

Average cost of home insurance in Indiana by dwelling amount

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $1,766 |

| $350,000 | $2,639 |

| $500,000 | $3,527 |

| $1,000,000 | $6,205 |

It's cheaper to insure a home in Indiana than it is in Illinois and Kentucky. These states may be more likely than Indiana to experience severe weather, which pushes up their monthly costs.

But Indiana's average rates are more expensive than rates in Michigan and Ohio, where $350,000 in home insurance coverage costs $2,246 per year and $2,015 per year, respectively.

Indiana homeowners insurance rates by city

Home insurance in Indianapolis costs an average of $3,020 per year for a policy with $350,000 in dwelling coverage.

Southport, which is just south of Indianapolis, has the most expensive average home insurance rates in Indiana, at $3,119 per year. This might be because central Indiana is known for its strong, gusty winds, which can cause damage to a home's roof and siding.

Shipshewana, a small town near the Michigan border, has the cheapest average home rates in the state at $2,195 per year.

Find Cheap Homeowners Insurance Quotes in Your Area

Cost of IN home insurance by city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Aberdeen | $2,443 | Allstate | $1,077 |

| Advance | $2,831 | Allstate | $1,018 |

| Akron | $2,442 | Allstate | $1,016 |

| Alamo | $2,716 | Allstate | $1,044 |

| Albany | $2,576 | Allstate | $964 |

| Albion | $2,369 | Allstate | $991 |

| Alexandria | $2,618 | Allstate | $1,025 |

| Altona | $2,247 | Allstate | $991 |

| Ambia | $2,700 | Allstate | $988 |

| Amboy | $2,462 | Allstate | $1,004 |

| Americus | $2,421 | Allstate | $1,055 |

| Amo | $2,882 | Allstate | $1,027 |

| Anderson | $2,605 | Allstate | $1,045 |

| Andrews | $2,381 | Allstate | $988 |

| Angola | $2,233 | Allstate | $972 |

| Arcadia | $2,622 | Allstate | $1,044 |

| Arcola | $2,226 | Allstate | $969 |

| Argos | $2,367 | Allstate | $961 |

| Arlington | $2,697 | Allstate | $1,135 |

| Ashley | $2,333 | Allstate | $972 |

| Athens | $2,489 | Allstate | $1,004 |

| Atlanta | $2,614 | Allstate | $1,018 |

| Attica | $2,680 | Allstate | $1,012 |

| Atwood | $2,350 | Allstate | $980 |

| Auburn | $2,221 | Allstate | $991 |

| Aurora | $2,559 | Allstate | $995 |

| Austin | $2,945 | Allstate | $1,005 |

| Avilla | $2,319 | Allstate | $991 |

| Avoca | $2,912 | Allstate | $1,079 |

| Avon | $2,869 | Allstate | $971 |

| Bainbridge | $2,719 | Allstate | $1,051 |

| Bargersville | $2,935 | Allstate | $1,123 |

| Bass Lake | $2,592 | Allstate | $944 |

| Batesville | $2,520 | Allstate | $995 |

| Bath | $2,457 | Allstate | $995 |

| Battle Ground | $2,434 | Allstate | $1,004 |

| Bedford | $2,911 | Allstate | $1,079 |

| Beech Grove | $2,992 | Allstate | $1,172 |

| Bellmore | $2,834 | Allstate | $1,038 |

| Bennington | $2,694 | Allstate | $995 |

| Bentonville | $2,552 | Allstate | $964 |

| Berne | $2,322 | Allstate | $980 |

| Bethlehem | $2,852 | Allstate | $1,097 |

| Beverly Shores | $2,635 | Allstate | $987 |

| Bicknell | $2,941 | Allstate | $1,029 |

| Bippus | $2,375 | Allstate | $980 |

| Birdseye | $2,870 | Allstate | $1,029 |

| Blanford | $2,867 | Allstate | $1,038 |

| Bloomfield | $2,845 | Allstate | $1,082 |

| Bloomingdale | $2,760 | Allstate | $1,022 |

| Bloomington | $2,597 | Allstate | $1,072 |

| Bluffton | $2,318 | Allstate | $980 |

Rates are for a policy with $350,000 of dwelling coverage.

What kind of home insurance do I need in Indiana?

Strong winds, heavy rains and cold temperatures are all common causes of damage in Indiana.

Knowing what is likely to damage your home can help you build your insurance policy with the coverage you'll need.

Does home insurance in Indiana cover wind?

Home insurance policies almost always cover damage caused by wind. Indiana can get windy, especially in the spring, when strong thunderstorms and tornadoes form. Rates for home insurance are likely higher in areas where strong winds are more common because damage is more likely.

According to the National Weather Service, Indiana recorded 67 tornadoes and 555 reports of high winds in 2025.

Even though wind damage is covered, it's always best to avoid damage if you can. To lessen the risk of wind damage, you can:

- Remove branches hanging over your house.

- Secure loose items, like patio furniture, before a storm.

- Get your roof inspected regularly.

If you lose power because of high winds, your policy might cover the cost of spoiled food in your fridge and freezer. Some policies include this coverage automatically, and sometimes you have to buy it as an add-on. Check your policy or talk with your agent to see if you have coverage.

Does Indiana home insurance cover snow and ice?

Snow and ice can cause damage to your home in several ways. Some of them are covered, while others usually aren't.

- Frozen and burst pipes: Home insurance typically covers the water damage caused by frozen and burst pipes. Cold temperatures can cause pipes in your home's outside walls to freeze and expand, which can crack the pipes. When the pipes thaw, the water can leak out of the cracks and cause damage.

- Breaking and falling trees: If ice and snow build up on a tree or branch near your home, it could fall and damage your house. Almost all home insurance policies would also cover trees or branches that fell on your home.

- Roof damage caused by weight: Ice and snow are heavy, and as they pile up on your roof, the weight can cause damage. Luckily, almost all types of home insurance cover this damage.

- Ice dams: These happen when the heat of your home melts the bottom layer of snow on your roof. Since the ice and snow near your gutters are still frozen, the melted water gets trapped and can't run off your roof. Instead, it can seep back into your home and cause water damage. Home insurance usually covers the damage to your roof and walls from ice dams.

Snow is common in most parts of the Hoosier state. Because of its location near Lake Michigan, northern Indiana often gets lake-effect snow, which is particularly heavy and wet. This type of snow can cause more damage to your roof as it piles up.

However, your insurance company might not pay a claim if the damage is caused by a lack of maintenance. For example, if you had a pipe freeze and burst last year but didn't fix it correctly, it could burst again. Home insurance probably wouldn't pay if the same pipe caused more damage.

Does Indiana home insurance cover flooding?

Basic home insurance does not cover flood damage. To have insurance coverage for flood damage, you have to buy a flood insurance policy.

Many parts of Indiana are prone to flooding, especially near the state's many lakes and rivers. The National Flood Insurance Program (NFIP) has handled 500 flood insurance claims in Indiana since 2020. Those floods caused nearly $24 million in damage.

You can buy flood insurance policies either through the NFIP or through a private insurance company. To get the best flood insurance, compare quotes from the NFIP to a few different private insurance companies.

How to save on home insurance in Indiana

The best way to get cheap home insurance in Indiana is to shop around and compare quotes.

That way, you can see what company has the cheapest rates for your specific home and coverage needs. You can also take some other steps to get a cheap policy.

Your roof is your home's first line of defense against wind, rain, snow and more. Not only will an updated roof lessen the chance of damage, but it'll also get you a discount with most insurance companies. | |

These sensors alert you if water is overflowing or leaking into an area where it shouldn't be. Some insurance companies will give you a discount for water sensors, especially in basements. Water damage in basements is common in Indiana. Preventing or minimizing it can save you and the insurance company money. | |

A home that is well taken care of is less likely to be damaged. That means it's less likely you will have to file a claim, which helps keep your rates down over time. Indiana's weather can be hard on homes, so inspecting your home often and keeping up with maintenance is important. |

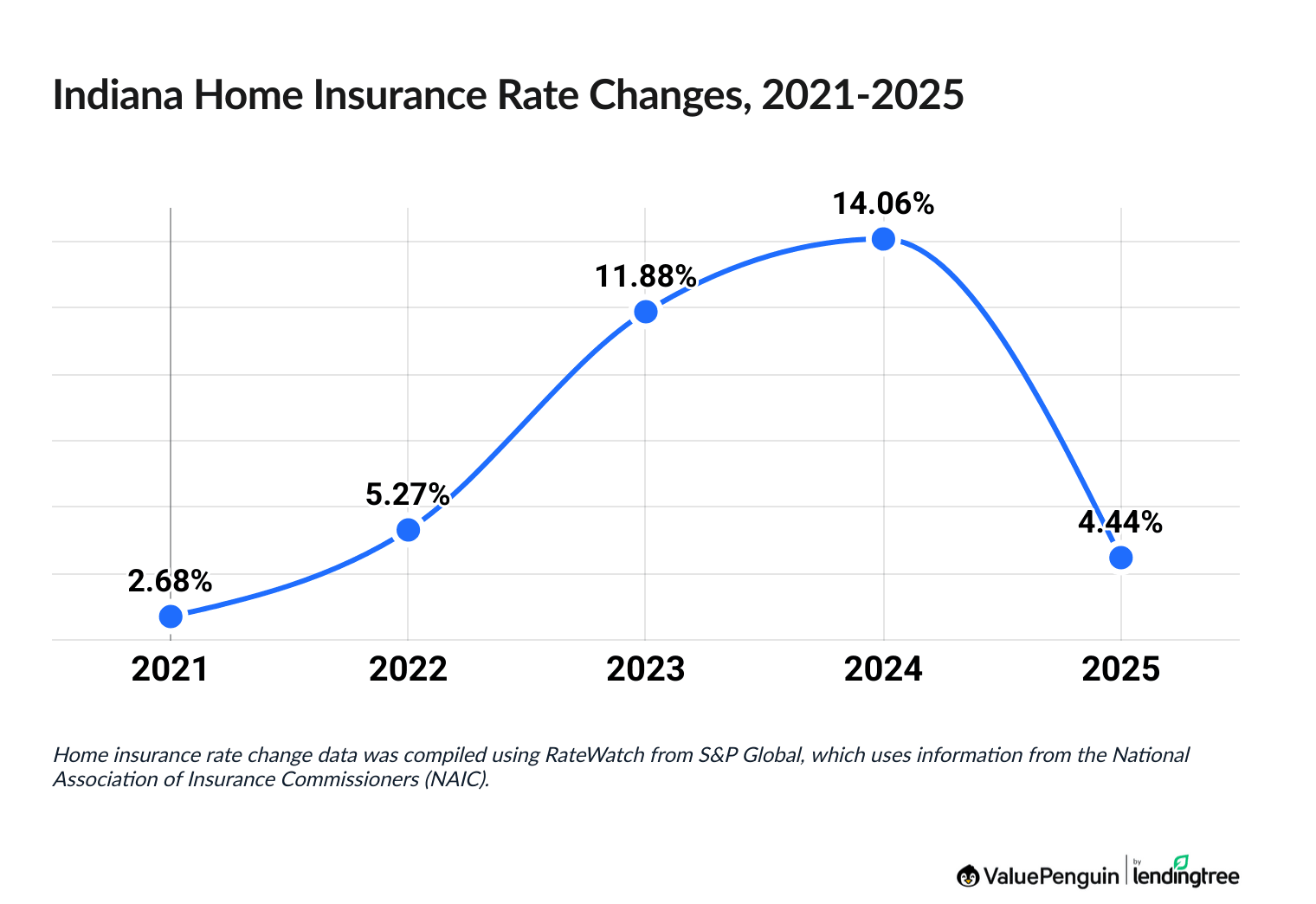

Are Indiana home insurance rates going up?

Home insurance prices have jumped 45.4% in Indiana over the last five years.

But the rate hikes seem to be slowing down. Prices only went up about 4.4% last year.

How much have home insurance rates in IN gone up between 2021 and 2025?

Year | Avg. rate increase |

|---|---|

| 2021 | 2.68% |

| 2022 | 5.27% |

| 2023 | 11.88% |

| 2024 | 14.06% |

| 2025 | 4.44% |

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

The jumps in prices are likely because of an increased cost of living. When homes are more expensive to repair, home insurance rates go up to help make sure companies have enough money to pay for claims.

Indiana Farmers Insurance had the largest increase, raising rates by over 90% between 2021 and 2025.

USAA had the smallest increase, but its prices still went up by nearly 26% in the last five years.

Frequently asked questions

How much is homeowners insurance in Indiana?

Home insurance in Indiana costs $2,639 per year for a house with $350,000 in dwelling coverage. Your cost will depend on where you live, how much coverage you need and what company you choose.

How much is home insurance in Indianapolis?

A $350,000 home in Indianapolis costs an average of $3,020 per year to insure. But that's just for the Indianapolis city limits. If you live in Carmel, for example, you'll pay an average of $2,648 per year. And in Fishers, the same house costs $2,757 per year, on average.

What company has the cheapest home insurance in Indiana?

Allstate has the cheapest home insurance in Indiana. A $350,000 house costs $1,026 per year, on average, with Allstate. That's less than half of the state average. Homes that need $500,000 or $1 million in dwelling coverage are also cheapest to insure with Allstate.

Methodology

To find the best home insurance in Indiana, ValuePenguin's experts got home insurance quotes from every residential ZIP code from 12 of the top companies in the state. Rates are for a 45-year-old married man with no home insurance claims on his record. The quotes are for a 49-year-old home with 2,011 square feet of living space, which is based on the average home in Indiana. New home data is for a home built in 2025.

Our experts used the following coverage limits to get average rates for a variety of home values:

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

ValuePenguin's analysis used insurance rate data from Quadrant Information Services. These rates were publicly sourced from insurance company filings and should be used for comparative purposes only — your own quotes may be different.

ValuePenguin's home insurance ratings combine complaint numbers from the NAIC, scores from J.D. Power's home insurance customer satisfaction and claims satisfaction surveys and ValuePenguin's own editorial ratings.

Sources:

About the Author

Senior Writer

Cate Deventer is a Senior Writer who specializes in health insurance, Medicare, auto and home insurance. She's been a licensed insurance agent since 2011.

She started her insurance career working as a customer service agent for State Farm. She later moved to an independent agency, where she worked with several insurance companies and hundreds of clients. She quoted policies, filed claims and answered insurance questions. In 2021, she pivoted her career and began writing about insurance for Bankrate. She moved to ValuePenguin in 2023 and began writing about health insurance and Medicare.

Cate has a passion for helping readers choose insurance to fit their needs. She enjoys knowing that her research and knowledge help people choose insurance products that make a positive difference in their lives.

How insurance helped Cate

Cate used her health insurance knowledge to navigate a surgery in 2023. Understanding how her policy worked let her focus on recovery instead of worrying about bills.

Expertise

- Health insurance

- Medicare & Medicaid

- Auto insurance

- Home insurance

- Life insurance

Credentials

- Licensed Life, Accident & Health Insurance Agent

- Licensed Property & Casualty Insurance Agent

Referenced by

- CBS

- NBC

- Wall Street Journal

Education

- BA, Theatre, Purdue University

- BA, English, Indiana University

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.