The Best and Cheapest Home Insurance in Minnesota in 2026

Farmers is the best and cheapest home insurance company for most people in MN, with an average rate of $1,950/year for a $350,000 policy. | ||

Home insurance in Minnesota costs an average of $2,774/year. That's about 16% higher than the national average rate. | ||

Homeowners in Minneapolis pay the highest average rates in the state, with a $350,000 policy coming in at $3,135/yr. |

Find Cheap Home Insurance Quotes in Minnesota

What's the best homeowners insurance in Minnesota?

What company has the cheapest home insurance in Minnesota?

Farmers has the cheapest home insurance in Minnesota for most people. A Farmers policy with $350,000 of coverage for your house costs $1,950 per year, on average.

Find Cheap Home Insurance Quotes in Minnesota

- Farmers has the cheapest average rates for homes with $350,000 or less in dwelling coverage. But if you need more coverage on your home, Auto-Owners or American Family may be a cheaper option.

- AAA has the cheapest average rates, at $2,047 per year, if you own a home in Minneapolis.

- Farmers also has cheap rates on new homes. A newly built home costs $1,273 per year to insure with Farmers. That's about 40% cheaper than average.

Best cheap home insurance in Minnesota by dwelling amount

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| Farmers | 4.0 out of 5 | $1,219 | |

| North Star Mutual | 4.5 out of 5 | $1,344 |

| Auto-Owners | 4.5 out of 5 | $1,399 | |

| AAA | 4.3 out of 5 | $1,408 | |

| Allstate | 4.0 out of 5 | $1,467 | |

| West Bend | 3.3 out of 5 | $1,486 |

| American Family | 2.3 out of 5 | $1,815 | |

| State Farm | 2.8 out of 5 | $2,258 | |

| Country Financial | 2.5 out of 5 | $3,541 | |

Key takeaways

- Home insurance rates in Minnesota have gone up by nearly 88% in the last five years.

- In 2025, home insurance rates in Minnesota went up by about 18%. That's the biggest increase for any state in the country.

- Travelers had the largest rate increase in Minnesota in 2025, raising prices by nearly 36%.

- But Nationwide has had the biggest increase over the last five years. Its rates are up more than 151% since 2021.

- AAA, Allstate and State Farm have had the lowest rate increases over the last five years. These companies raised rates by less than 75%.

Best and cheapest home insurance for most people in Minnesota: Farmers

-

Annual cost$1,950Average rate for a $350,000 home

-

Monthly cost$163Average rate for a $350,000 home

-

LowCustomer complaints

Best homeowners insurance in Minneapolis: AAA

-

Annual cost$2,284Average rate for a $350,000 home

-

Monthly cost$190Average rate for a $350,000 home

-

LowCustomer complaints

Best for high-value homes in Minnesota: American Family

-

Annual cost$3,244Average rate for a $350,000 home

-

Monthly cost$270Average rate for a $350,000 home

-

HighCustomer complaints

What are the top-rated home insurance companies in Minnesota?

The best-rated home insurance companies in Minnesota include Auto-Owners and North Star Mutual.

Both companies have good coverages and discounts. Both companies have low rates of complaints, according to the National Association of Insurance Commissioners (NAIC). This means most homeowners are happy with the service they get from these companies.

Company |

Rating

|

Complaints

|

|---|---|---|

| Auto-Owners | 4.5 out of 5 | Low |

| North Star Mutual | 4.5 out of 5 | Average |

| AAA | 4.3 out of 5 | Low |

| Allstate | 4.0 out of 5 | Average |

| Farmers | 4.0 out of 5 | Low |

| Chubb | 3.8 out of 5 | Low |

| West Bend | 3.3 out of 5 | Low |

| State Farm | 2.8 out of 5 | Average |

| Country Financial | 2.5 out of 5 | Low |

| American Family | 2.3 out of 5 | High |

What's the average home insurance cost in MN?

In Minnesota, home insurance costs $2,774 per year, on average, for a policy with $350,000 in dwelling coverage.

That's about 16% higher than the national average home insurance rate of $2,395 per year.

Average cost of home insurance in MN

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $1,771 |

| $350,000 | $2,774 |

| $500,000 | $3,896 |

| $1 million | $6,911 |

Home insurance in Minnesota is cheaper than coverage in nearby South Dakota and Iowa. In these states, $350,000 in dwelling coverage costs more than $3,000 per year, on average. That's possibly because wind damage is more common in South Dakota and Iowa than it is in Minnesota.

But the same coverage is cheaper in North Dakota and Wisconsin, where a policy costs $2,460 and $1,679 per year, on average, respectively.

Cost of Minnesota home insurance by city

Minneapolis has the most expensive home insurance rates in Minnesota, at $3,135 per year on average.

That's 13% more than the state average. But you may be able to get a cheaper policy if you shop around. AAA has the cheapest average rates in Minneapolis, at $2,047 per year for $350,000 in dwelling coverage.

Goodridge, a tiny town in northern Minnesota, has the cheapest home insurance rates in the state, at an average of $2,529 per year.

Farmers and Auto-Owners tend to be the cheapest companies in most cities, but North Star Mutual and AAA are also cheap options.

Find Cheap Home Insurance Quotes in Minnesota

Cost of MN home insurance by city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Ada | $2,622 | Auto-Owners | $1,862 |

| Adams | $2,646 | Auto-Owners | $1,916 |

| Adolph | $2,601 | Farmers | $1,626 |

| Adrian | $2,824 | Auto-Owners | $2,023 |

| Afton | $2,995 | Farmers | $2,114 |

| Ah Gwah Ching | $2,665 | Farmers | $1,739 |

| Aitkin | $2,740 | Farmers | $1,675 |

| Akeley | $2,629 | Farmers | $1,789 |

| Albany | $2,679 | Farmers | $1,833 |

| Albert Lea | $2,732 | Auto-Owners | $1,949 |

| Alberta | $2,766 | Farmers | $2,020 |

| Albertville | $2,895 | Farmers | $1,784 |

| Alborn | $2,596 | Farmers | $1,604 |

| Alden | $2,741 | Auto-Owners | $1,993 |

| Aldrich | $2,716 | Farmers | $1,832 |

| Alexandria | $2,723 | Farmers | $1,931 |

| Almelund | $2,904 | Farmers | $1,954 |

| Alpha | $2,807 | Auto-Owners | $1,925 |

| Altura | $2,657 | Auto-Owners | $1,795 |

| Alvarado | $2,585 | Auto-Owners | $1,655 |

| Amboy | $2,715 | Auto-Owners | $1,970 |

| Andover | $3,058 | Farmers | $1,946 |

| Angle Inlet | $2,564 | Auto-Owners | $1,644 |

| Angora | $2,549 | Farmers | $1,565 |

| Annandale | $2,903 | Farmers | $1,919 |

| Anoka | $3,048 | Farmers | $1,917 |

| Apple Valley | $2,932 | Farmers | $2,138 |

| Appleton | $2,777 | North Star Mutual | $2,110 |

| Arco | $2,855 | North Star Mutual | $2,110 |

| Arden Hills | $3,016 | Farmers | $2,195 |

| Argyle | $2,582 | Auto-Owners | $1,652 |

| Arlington | $2,758 | North Star Mutual | $2,110 |

| Arnold | $2,591 | Farmers | $1,446 |

| Ashby | $2,714 | Farmers | $1,762 |

| Askov | $2,771 | Farmers | $1,639 |

| Atwater | $2,770 | Farmers | $1,985 |

| Audubon | $2,630 | Farmers | $1,935 |

| Aurora | $2,564 | Farmers | $1,599 |

| Austin | $2,682 | Auto-Owners | $1,896 |

| Avoca | $2,828 | North Star Mutual | $2,110 |

| Avon | $2,682 | Farmers | $1,813 |

| Babbitt | $2,548 | Farmers | $1,524 |

| Backus | $2,643 | Farmers | $1,746 |

| Badger | $2,576 | Auto-Owners | $1,648 |

| Bagley | $2,589 | Farmers | $1,654 |

| Balaton | $2,853 | North Star Mutual | $2,110 |

| Barnesville | $2,615 | Farmers | $1,906 |

| Barnum | $2,689 | Farmers | $1,598 |

| Barrett | $2,732 | Auto-Owners | $1,981 |

| Barry | $2,786 | North Star Mutual | $2,110 |

| Battle Lake | $2,703 | Farmers | $1,977 |

| Baudette | $2,553 | Farmers | $1,599 |

Rates are for a policy with $350,000 of dwelling coverage.

What kind of home insurance coverage do I need in Minnesota?

If you live in Minnesota, make sure your home insurance covers damage caused by wind and snow.

You may also want to consider buying a flood insurance policy because standard home insurance doesn't cover flood damage.

Does Minnesota home insurance cover wind damage?

Standard home insurance policies usually cover damage from high winds. High winds can easily damage roofs and siding. Plus, the damage they cause can sometimes let rain and snow inside.

In 2025, Minnesota experienced 351 episodes of high winds, according to the NOAA/National Weather Service Storm Prediction Center.

However, if your roof or siding is in bad condition, it's possible your home insurance won't cover the damage. This is called an "exclusion," and it's a good idea to make sure your roof and siding aren't excluded. You should also check to see if you have a separate wind deductible, which is usually higher than the deductible for other types of damage.

Does home insurance in MN cover snow and ice damage?

Damage caused by snow and ice is almost always included in your home insurance policy.

But it's a good idea to check your policy to be sure, especially if you live in northern Minnesota. Snow there can sometimes pile up to heights of more than two or three feet. That can be incredibly heavy and could cause damage to your roof.

Plus, low temperatures could cause your pipes to freeze and burst. If that happens, the resulting water damage is usually covered, but the damage to the pipe isn't.

Does Minnesota home insurance cover flooding?

Home insurance almost never covers flooding. To have coverage for floods, you need to buy a separate flood insurance policy.

The Federal Emergency Management Agency (FEMA) had paid out more than $17 million in damages for nearly 600 flood claims in Minnesota since 2015. Flooding is more common in southeast Minnesota, near Minneapolis, but it can happen anywhere in the state.

Tips to save money on your Minnesota home insurance policy

To get the cheapest home insurance policy, you should shop around, bundle your policies and consider increasing your deductible.

Every company has different home insurance rates, and shopping around can save you thousands of dollars. In Minnesota, the difference between the most expensive company (Country Financial) and the least expensive company (Farmers) for $350,000 in dwelling coverage is $3,132 per year. | |

Bundling your car and home insurance just means getting your policies from the same company. Bundling discounts are usually pretty big and can substantially lower both your car and home insurance rates. | |

A higher home insurance deductible means a lower annual rate. Increasing your deductible can be a useful tool to get cheaper home insurance, but you should always choose a deductible you can afford to pay. If your deductible is too high, you might have trouble paying it if you need to file a claim. |

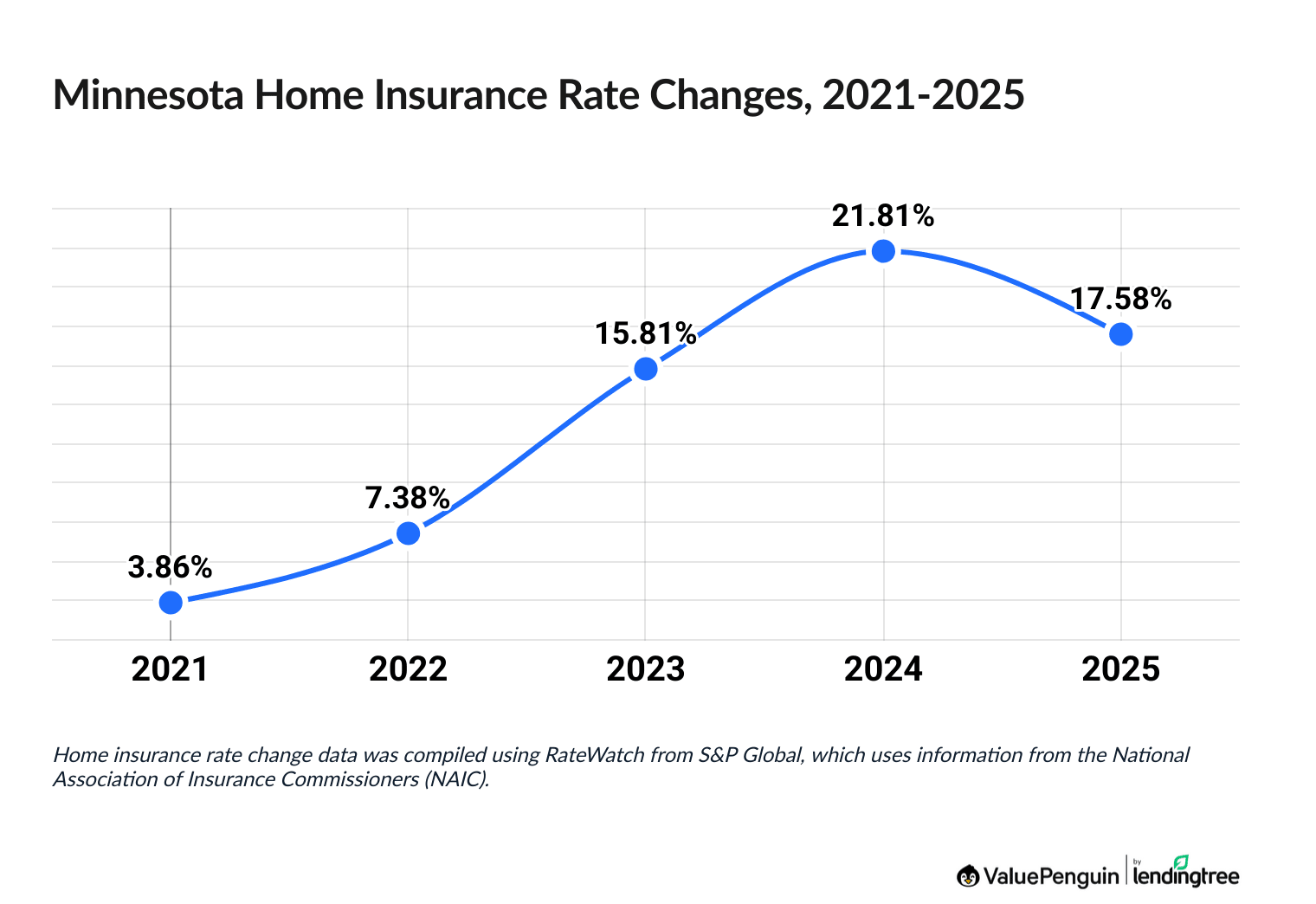

Surging Minnesota home insurance costs

Home insurance prices are up nearly 88% in Minnesota over the last five years.

In 2025, Minnesota had the largest rate increase in the country, at 17.58%.

Minnesota home insurance rate changes, 2021-2025

Year | Avg. rate increase |

|---|---|

| 2021 | 3.86% |

| 2022 | 7.38% |

| 2023 | 15.81% |

| 2024 | 21.81% |

| 2025 | 17.58% |

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Travelers raised rates the most in Minnesota in 2025, with prices increasing nearly 36%.

But Nationwide has raised its rates the most in the last five years. A Nationwide policy costs 151% more now than in 2021.

AAA has had the smallest rate change in the last five years, but its rates are still 27% higher than they were in 2021.

Frequently asked questions

What's the best and cheapest homeowners insurance in Minnesota?

Farmers is the best home insurance company in Minnesota for most people. It has cheap rates, with $350,000 in dwelling coverage coming in at $1,950 per year. Plus, Farmers has lots of discounts to help you get an even cheaper rate. Other cheap companies include AAA and Auto-Owners.

What's the best homeowners insurance in Minneapolis?

AAA has the best home insurance in Minneapolis. The company's rates are cheap

What is the average homeowners insurance cost in Minnesota?

On average, home insurance in Minnesota costs $2,774 per year for a policy with $350,000 in dwelling coverage. Your rates vary depending on the company you pick, your age, the details of your home, and whether or not you've filed any home claims in the past.

Methodology

ValuePenguin collected quotes from 10 of the top home insurance companies in Minnesota across 895 residential ZIP codes. Rates are for a 45-year-old married man with no history of insurance claims. The quotes are for a 2,026 square foot home built 46 years ago, which is representative of the average home in Minnesota. New home data is for a home built in 2025.

The quotes are for policies with the following coverage limits:

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

ValuePenguin's analysis uses insurance rate data from Quadrant Information Services. Quadrant's rates were taken from public filings and should only be used for comparative purposes. Your rates will be different depending on your circumstances.

Home insurance ratings use average rates, coverage offerings, available discounts, complaint data from the National Association of Insurance Commissioners (NAIC), and the J.D. Power customer satisfaction and claims satisfaction surveys.

Sources:

About the Author

Senior Writer

Cate Deventer is a Senior Writer who specializes in health insurance, Medicare, auto and home insurance. She's been a licensed insurance agent since 2011.

She started her insurance career working as a customer service agent for State Farm. She later moved to an independent agency, where she worked with several insurance companies and hundreds of clients. She quoted policies, filed claims and answered insurance questions. In 2021, she pivoted her career and began writing about insurance for Bankrate. She moved to ValuePenguin in 2023 and began writing about health insurance and Medicare.

Cate has a passion for helping readers choose insurance to fit their needs. She enjoys knowing that her research and knowledge help people choose insurance products that make a positive difference in their lives.

How insurance helped Cate

Cate used her health insurance knowledge to navigate a surgery in 2023. Understanding how her policy worked let her focus on recovery instead of worrying about bills.

Expertise

- Health insurance

- Medicare & Medicaid

- Auto insurance

- Home insurance

- Life insurance

Credentials

- Licensed Life, Accident & Health Insurance Agent

- Licensed Property & Casualty Insurance Agent

Referenced by

- CBS

- NBC

- Wall Street Journal

Education

- BA, Theatre, Purdue University

- BA, English, Indiana University

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.