What Are Your Medicare Coverage Options?

There are several types of Medicare you can choose from, including Original Medicare and Medicare Advantage.

Compare Medicare Plans in Your Area

Original Medicare is also called Parts A and B, while Medicare Advantage, which bundles your coverage into one plan, is called Part C. Additional coverage, such as coverage for prescription medications, can be added on to Original Medicare, while Medicare Advantage is an all-in-one bundle.

What are your Medicare options?

There are four "parts" of Medicare — A, B, C and D — plus an additional category of Medicare Supplement plans.

- Medicare Part A: Hospital and inpatient coverage

- Medicare Part B: Doctors and outpatient coverage

- Medicare Part C: Bundled plans with multiple types of coverage

- Medicare Part D: Prescription drug coverage

- Medicare Supplement: Add-on coverage to cut your medical costs with Parts A and B

How are the different Medicare options combined?

Original Medicare offers a mix-and-match style of coverage, while Medicare Advantage plans bundle your coverage together.

With Original Medicare, you start with Parts A and B, which both come from the federal government. Then, you can add extra plans, such as Part D or Medicare Supplement (Medigap), to get more coverage.

If you opt for a Medicare Advantage plan, all your coverage is bundled into one policy that comes from a private insurance company.

Original Medicare

-

Parts A and B: Basic medical benefits

- Part D: Add-on prescription coverage

- Medigap: Add-on medical benefits

Medicare Advantage

- Part C: Includes Parts A and B and usually comes with coverage for prescriptions. Most plans have extra perks, like coverage for vision, dental and hearing care.

Original Medicare plus Part D and Medigap gives you the best coverage, but it can be expensive.

Medicare Advantage plans are a cheaper option, at $27 per month, on average. They might be fine for people who don't need as much medical care. But as you age and face more health issues, Medicare Advantage plans can leave you with higher out-of-pocket costs.

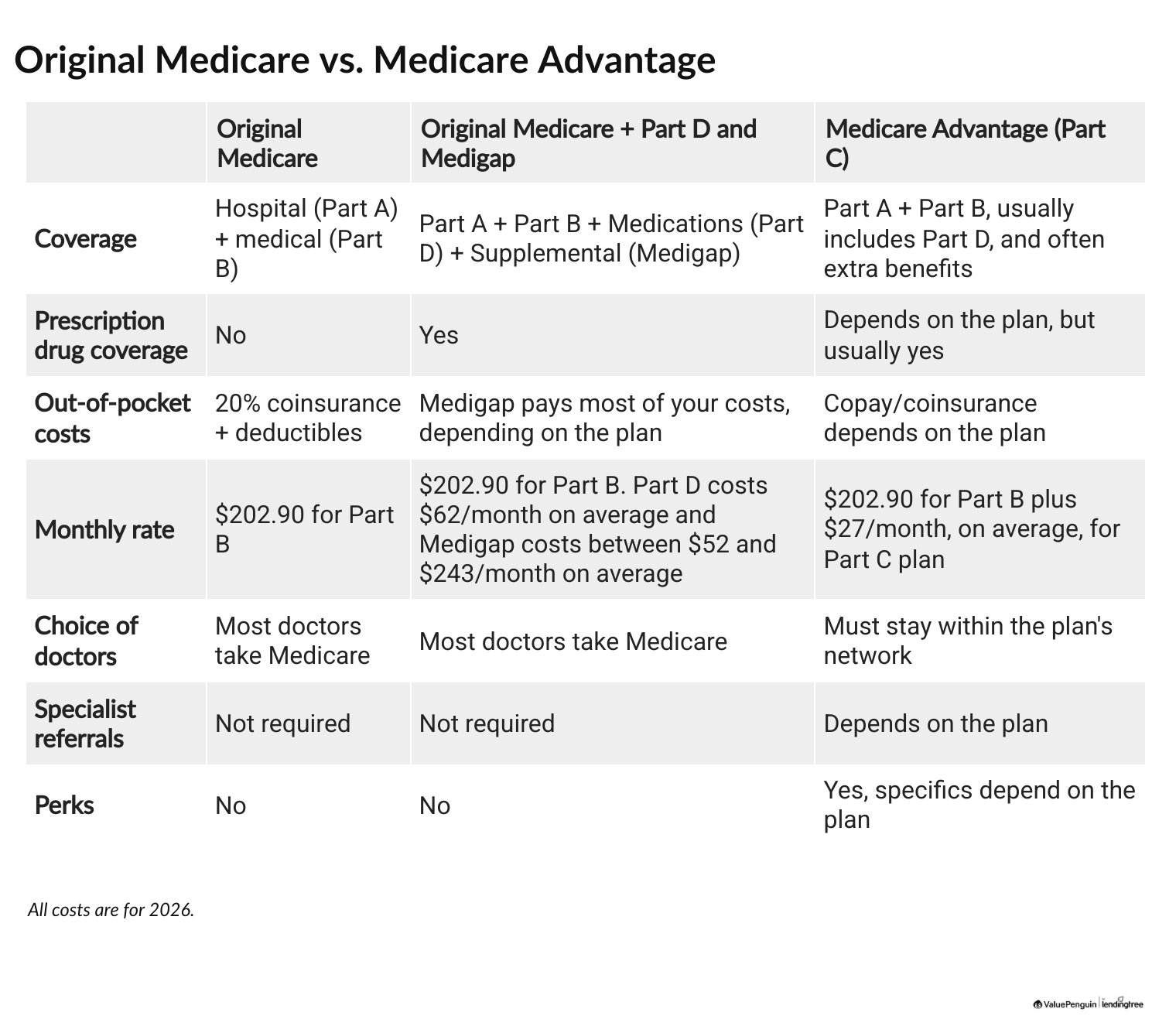

Original Medicare vs. Medicare Advantage

Part A + B

| A + B + D + Medigap |

Part C

| ||

|---|---|---|---|---|

| Hospital | ||||

| Medical | ||||

| Drugs | Usually | |||

| Monthly cost | $202.90 | $317-$508 | $230 | |

| OOP costs | High | Low | Med | |

| Use any doctor | ||||

| Need referrals | Depends | |||

| Extras | Usually |

All costs are for 2026.

Medicare Advantage plans are a type of plan called "managed care," which means an insurance company sets prices for medical care. This is similar to how regular health insurance plans work. You'll usually have extra perks like coverage for dental and vision care, but you have to stay within a certain network of doctors. You may also run into issues like needing preauthorization before expensive procedures. However, Medicare Advantage plans are usually a cheaper option than stacking coverage types with Original Medicare.

Original Medicare, on the other hand, is what's called a "fee-for-service" plan. This means that Medicare sets the cost of medical care, and doctors who take Medicare agree to the cost for each service. Original Medicare gives you access to most of the doctors in the country. The extra plans you add to Original Medicare can be expensive, but ultimately they'll pay for most of your medical bills.

Learn more: Medicare Advantage vs. Medigap

What are the different Medicare coverage options?

Each part of Medicare can have multiple plans available. While you don't have to pick specific options for Parts A and B, you do have to choose a plan with Medicare Advantage (Part C), Part D and Medigap.

Part A: Hospitalization

Medicare Part A, part of "Original Medicare," covers hospitalization and care that you get when you have to stay in the hospital. The government provides the coverage, which means the benefits are the same no matter where you live.

You don't need to make any coverage decisions or choose any plans with Part A. Medicare Part A is free for 99% of enrollees. The most important thing to remember is to enroll on time to avoid penalties. For most people, you get coverage when you turn 65.

Learn more: How does Medicare Part A work?

Part B: Doctors and outpatient care

Medicare Part B covers you when you go to the doctor but aren't staying in the hospital. The coverage is the same no matter where you live. Part B is the second half of "Original Medicare."

You won't have any decisions about plans to get Part B coverage. However, the cost of Part B can vary based on your situation. The standard rate is currently $202.90 per month, which is what most people pay. High-income earners pay more each month, while people with low incomes can qualify for savings.

There is also a penalty for enrolling late in Part B, except in circumstances when you're still working past age 65 and have coverage through your job. So make sure you sign up when you're first eligible.

Learn more: How does Medicare Part B work?

Part C (Medicare Advantage): Bundled coverage

Medicare Advantage plans are all-in-one options that combine multiple types of coverage. Instead of coming from the government, these plans are sold by private insurance companies.

With Medicare Advantage, you have to choose a specific plan to buy. Depending on where you live, there's usually a wide variety of plan options, including different companies and coverage levels. The plan you choose will determine how much you pay for medical care and which doctors will be the cheapest.

The available plans change based on where you live, and on average, shoppers can choose from 21 different plans.

To start comparing your options, use Medicare.gov or a plan comparison tool to see what plans are offered in your area. Compare companies to find a plan that has affordable rates, good service and your preferred doctors in the network. Remember, if you have a Medicare Advantage plan, you can't add a stand-alone Part D plan or Medicare Supplement plan.

Learn more: How does Medicare Part C work?

Among the five most popular insurers selling Medicare Advantage plans, Aetna has the cheapest rates and Kaiser Permanente has the highest quality ratings.

Company | Medicare.gov rating | Average monthly cost | ||||

|---|---|---|---|---|---|---|

| Kaiser Permanente | 4.5 out of 5 | $49 | ||||

| AARP/UHC | 4.0 out of 5 | $26 | ||||

| Blue Cross Blue Shield | 4.0 out of 5 | $48 | Aetna | 3.5 out of 5 | $19 | |

| Humana | 3.5 out of 5 | $22 |

Learn more about ValuePenguin's picks for the Best Medicare Advantage plans.

Compare Medicare Plans in Your Area

Part D: Prescriptions

Medicare Part D plans are sold by private insurance companies, and your plan options depend on where you live.

Part D plans give you prescription drug coverage, something that isn't automatically included in Original Medicare (Parts A and B). If you choose a Medicare Advantage plan, you won't be able to buy a stand-alone Part D plan. However, most Medicare Advantage plans come with prescription drug coverage built in.

All Part D plans have to cover some medications in certain key categories, like medications to treat depression or cancer. However, the specific medications you have coverage for depend on the plan you buy. When you're comparing options, make sure you look at each plan's list of covered medications, called a formulary, to make sure your medications are covered.

Your Part D plan options depend on where you live, and the first step when shopping is to find out which plans are offered in your area. When you're shopping, look at each plan's total spending, called the out-of-pocket maximum. You'll never spend more than $2,100 on covered medications. But if you need expensive drugs or take more than one medication, choosing a plan with a lower out-of-pocket maximum helps you keep your costs down.

Learn more: How does Medicare Part D work?

Wellcare has the best-rated Part D plans and the cheapest rates. Human and Aetna are also decent options.

Company | Medicare.gov rating | Average monthly cost | |

|---|---|---|---|

| Wellcare | 3.5 out of 5 | $8 | |

| Humana | 3.0 out of 5 | $54 | |

| Aetna | 3.0 out of 5 | $69 | |

| Blue Cross Blue Shield | 3.0 out of 5 | $119 | |

| AARP/UHC | 2.5 out of 5 | $90 |

Learn more about our picks for the Best Medicare Part D plans.

Medicare Supplement (Medigap): Extra coverage

Medicare Supplement insurance (Medigap) lowers what you pay for medical care by paying for most of the costs that Original Medicare leaves you with.

There are 10 plan options available, named A through N. The coverage for a given plan letter is the same no matter what company you choose. For example, Plan G from Blue Cross Blue Shield gives you the same coverage as Plan G from Mutual of Omaha. This makes it easier to compare Medicare Supplement plans than it is to compare many other types of Medicare, because you can focus just on the price of a plan and the company's customer service.

It's important to sign up for Medigap when you're first eligible, when you turn 65. During this time, your application can’t be denied and you won’t pay more because of your medical history.

AARP/UnitedHealthcare (UHC) has the best Medicare Supplement plans, but Blue Cross Blue Shield and Mutual of Omaha are also good options.

Company | Plans offered | Average cost of Plan G | |

|---|---|---|---|

| AARP/UHC | A, B, C, D, F, G, K, L, N, high-deductible G | $177 | |

| Blue Cross Blue Shield | A, B, C, D, F, G, K, L, M, N, high-deductible F and G | $189 | |

| Mutual of Omaha | A, B, C, D, F, G, M, N, high-deductible F and G | $207 |

Monthly rates for a 65-year-old female nonsmoker

Learn more about our picks for the best Medicare Supplement plans.

Compare Medicare Plans in Your Area

How to pick the right Medicare options for you

Choosing the right Medicare options means you have to consider both your current and future medical needs.

That's because you'll often pay higher rates if you wait to get certain types of Medicare, like Medigap. Deciding early what kind of coverage you want in the future can help you choose a combination of plans that work for you now and as you age.

Think about your current medical needs. Are you generally healthy and don't need much medical care? A Medicare Advantage plan could be a good option, especially if you find one that has your doctors in its network. But if you need frequent, complex or expensive medical care, staying on Original Medicare and buying separate Part D and Medigap plans gives you better coverage, even though it's more expensive.

Consider your future medical needs. No one can predict the future, but it can be helpful to try to anticipate what kind of medical attention you may need in the future. Do you have a family history of serious illness, for example, or do you have any current medical conditions that could create problems down the road? And regardless of your medical needs, would you prefer the peace of mind knowing you have better coverage should something serious happen?

Overall, sticking with Original Medicare and getting a Part D plan for medications and a Medicare Supplement plan to fill in gaps in coverage means you'll pay the least amount when you go to the doctor or need medical care. But it's important to decide early if you want a Medicare Supplement plan. It's cheaper and easier to get a plan when you're first eligible at age 65. Let's say you choose a Medicare Advantage plan when you first turn 65 but later decide you want a Medigap plan instead. You may not be able to afford a Medigap plan then because prices go up as you age, which could leave you stuck in a plan that doesn't work for you anymore.

Decide on your monthly budget. No matter what plan combination you choose, you'll have to pay the monthly rate for Part B, which is $202.90 in 2026. Most people don't pay for Part A. Medicare Advantage, Medigap and Part D plans all have their own monthly rates, too.

In general, if your budget is tight, consider Medicare Advantage. Many plans have no monthly rate, which means you'd only pay your Part B rate each month. If you can afford higher rates, consider Original Medicare with a Part D and Medigap plan added on.

Rates vary depending on where you live, the company you're considering and the specifics of the plan. Before deciding that you can't afford a certain plan type, take the time to look at all the options in your area. You might be surprised at the range of options.

Frequently asked questions

What are the four types of Medicare?

Medicare is split into four parts: Part A, Part B, Part C and Part D. However, you can't have all four parts at once. Parts A and B are called "Original Medicare," and they pay for your hospital and doctor visit costs. You can add Part D, which covers prescription medications, to Original Medicare. You can also add a Medicare Supplement plan for more coverage. Part C, also called Medicare Advantage, rolls Parts A and B into one plan, and it usually includes coverage for prescription medications, too.

What is the best Medicare option?

Original Medicare plus a Part D plan and a Medigap plan is the best combination of Medicare options for most people. This combination of plans pays for most of your medical costs, which means you'll pay little or nothing toward your medical bills. Medicare Advantage plans can be a decent option if you need a cheaper plan. However, if you get a Medicare Advantage plan, you have to use the plan's network of doctors and you may face issues like needing prior authorization to see a specialist or to have certain procedures.

How do I get dental and vision coverage with Medicare?

The only way to get dental and vision coverage from Medicare is to get a Medicare Advantage plan. Original Medicare doesn't usually cover dental or vision care except in specific situations. But most Medicare Advantage plans include coverage for dental, vision and hearing care. However, don't pick a plan just because it has vision or dental coverage. Make sure you consider all your medical needs before you buy a plan.

Sources and methodology

Medicare Advantage and Medicare Part D costs and star ratings are averages of nationwide data and are based on public use files from the Centers for Medicare & Medicaid Services (CMS).

Medicare Supplement rates are from actuarial data for private insurance companies. Average rates are for a 65-year-old nonsmoking woman. The rates are the averages for when a person first becomes eligible for Medicare and health isn't used to set rates.

All plan data is based on 2026 rates.

About the Author

Senior Writer

Cate Deventer is a Senior Writer who specializes in health insurance, Medicare, auto and home insurance. She's been a licensed insurance agent since 2011.

She started her insurance career working as a customer service agent for State Farm. She later moved to an independent agency, where she worked with several insurance companies and hundreds of clients. She quoted policies, filed claims and answered insurance questions. In 2021, she pivoted her career and began writing about insurance for Bankrate. She moved to ValuePenguin in 2023 and began writing about health insurance and Medicare.

Cate has a passion for helping readers choose insurance to fit their needs. She enjoys knowing that her research and knowledge help people choose insurance products that make a positive difference in their lives.

How insurance helped Cate

Cate used her health insurance knowledge to navigate a surgery in 2023. Understanding how her policy worked let her focus on recovery instead of worrying about bills.

Expertise

- Health insurance

- Medicare & Medicaid

- Auto insurance

- Home insurance

- Life insurance

Credentials

- Licensed Life, Accident & Health Insurance Agent

- Licensed Property & Casualty Insurance Agent

Referenced by

- CBS

- NBC

- Wall Street Journal

Education

- BA, Theatre, Purdue University

- BA, English, Indiana University

Editorial Note: We are committed to providing accurate content that helps you make informed financial decisions. Our partners have not endorsed or commissioned this content.