The Best and Cheapest Homeowners Insurance in Kansas (2026)

State Farm has the best home insurance in Kansas, with an average rate of $1,732/yr for $350,000 in coverage. | ||

Kansas home insurance costs an average of $4,095/yr. That's the fourth-highest rate in the country. | ||

Homeowners in Kansas City pay an average of $3,444/yr for $350,000 in dwelling coverage. |

State Farm has the best home insurance in Kansas, with an average rate of $1,732/yr for $350,000 in coverage. | ||

Home insurance in KS costs $4,095/yr, on average. But the average rate in Kansas City is $3,444/yr. |

Find Cheap Home Insurance Quotes in Kansas

What company has the best homeowners insurance in Kansas?

Who has the cheapest home insurance in Kansas?

State Farm has the cheapest home insurance in Kansas for most people. A policy with $350,000 in dwelling coverage costs $1,732 per year, on average, with State Farm.

Find Cheap Home Insurance Quotes in Kansas

- State Farm has the cheapest average home insurance rates in Kansas across several levels of coverage. But just because State Farm is cheap on average doesn't mean it'll be the cheapest for you. It's always a good idea to shop around and compare quotes.

- Shelter and Farmers also often have cheap rates.

- Shelter has the best coverage options in Kansas. Even though it costs a bit more than State Farm, it could be worth it if you want to personalize your policy.

Cheapest home insurance in Kansas by dwelling coverage amount

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| State Farm | 3.5 out of 5 | $1,245 | |

| Shelter | 4.5 out of 5 | $1,715 | |

| Farmers | 3.5 out of 5 | $1,902 | |

| Auto-Owners | 4.0 out of 5 | $2,588 | |

| Nationwide | 2.8 out of 5 | $2,806 | |

| Allstate | 3.3 out of 5 | $3,179 | |

| Farm Bureau | 2.3 out of 5 | $3,214 | |

| American Family | 2.0 out of 5 | $4,030 | |

Key takeaways

- Home insurance rates in Kansas have gone up by about 42% in the last five years.

- Liberty Mutual has had the biggest rate hikes. Rates for Liberty Mutual policies are up 81% since 2021.

- Shelter raised rates the least. A policy from Shelter costs about 11% more today than it did five years ago.

- Kansas deals with rough summer weather, including high winds, tornadoes and hail. Home insurance usually covers damage from wind, tornadoes and hail, but it's a good idea to check with your agent or company to make sure.

Best home insurance in Kansas for most people: State Farm

-

Annual cost$1,732Average rate for a $350,000 home

-

Monthly cost$144Average rate for a $350,000 home

-

AverageCustomer complaints

Best home insurance coverage options in Kansas: Shelter

-

Annual cost$2,967Average rate for a $350,000 home

-

Monthly cost$247Average rate for a $350,000 home

-

LowCustomer complaints

Best home insurance claims process in Kansas: Auto-Owners

-

Annual cost$3,591Average rate for a $350,000 home

-

Monthly cost$299Average rate for a $350,000 home

-

LowCustomer complaints

Auto-Owners has the best home insurance claims service in Kansas.

According to J.D. Power, Auto-Owners gets one of the highest scores for claims satisfaction among home insurance companies in Kansas.

Claims service is an important part of choosing a home insurance company, especially in a state like Kansas, where home damage is more likely. Picking a company with good claims service could mean your home is repaired faster after it's damaged, and that the repair process is smoother.

Auto-Owners also has excellent coverage options and discounts to help you personalize your policy. And Auto-Owners works with local independent agents, who can help you pick the right coverage for you.

What are the top-rated home insurance companies in Kansas?

Shelter and Auto-Owners are the top-rated home insurance companies in Kansas.

Both companies get fewer complaints than expected, according to the National Association of Insurance Commissioners (NAIC). This means customers are usually happy with their experiences.

Company |

Rating

|

Complaints

|

|---|---|---|

| Shelter | 4.5 out of 5 | Low |

| Auto-Owners | 4.0 out of 5 | Low |

| Farmers | 3.5 out of 5 | Average |

| State Farm | 3.5 out of 5 | Average |

| Allstate | 3.3 out of 5 | Average |

| Nationwide | 2.8 out of 5 | High |

| Farm Bureau | 2.3 out of 5 | Low |

| American Family | 2.0 out of 5 | High |

What's the average cost of homeowners insurance in Kansas?

Home insurance in Kansas costs $4,095 per year, on average, for $350,000 in dwelling coverage.

Kansas has the fourth-highest average home insurance rate in the country. Rates are only higher in nearby Oklahoma, Nebraska and Colorado.

Average cost of home insurance in Kansas by dwelling amount

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $2,585 |

| $350,000 | $4,095 |

| $500,000 | $5,562 |

| $1 million | $10,304 |

The home insurance rates are likely high in Kansas because of how common wind and tornado damage is in the state. Rates in "Tornado Alley" tend to be high. In Oklahoma, home insurance costs $5,298 per year, on average. In Nebraska, the average is $4,956 per year, and in Colorado, it's $4,310 per year. But in Missouri, to the east of Kansas, home insurance costs $2,641 per year.

However, Tornado Alley has begun to shift as climate patterns change. The most severe weather now tends to happen in the southeastern parts of the U.S. If severe weather becomes less common in Kansas, home insurance rates could go down.

Kansas home insurance rates by city

Home insurance in Kansas City costs $3,444 per year, on average.

That's about 16% less than the state average. Similarly, in the state capital of Topeka, the average cost of home insurance is $3,665 per year, which is 11% cheaper than average. But home insurance in Wichita, the state's largest city, costs $4,799 per year, on average, which is 17% more than average.

Lawrence, a city to the southwest of Kansas City and home to the University of Kansas, has the cheapest home insurance in Kansas, with an average rate of $3,133 per year. Rush Center, a small town in West Central Kansas, has the most expensive home insurance, with an average rate of $5,103 per year.

In general, homeowners in central and western Kansas, the more rural part of the state, pay higher rates than homeowners in the eastern part of the state.

Cost of KS home insurance by city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Abbyville | $4,534 | State Farm | $1,663 |

| Abilene | $3,939 | State Farm | $1,742 |

| Admire | $3,752 | State Farm | $1,663 |

| Agenda | $3,784 | State Farm | $1,663 |

| Agra | $4,674 | State Farm | $1,886 |

| Albert | $4,884 | State Farm | $1,663 |

| Alden | $4,424 | State Farm | $1,871 |

| Alexander | $5,023 | State Farm | $1,663 |

| Allen | $3,726 | State Farm | $1,733 |

| Alma | $3,741 | State Farm | $1,690 |

| Almena | $4,775 | State Farm | $1,814 |

| Alta Vista | $3,787 | State Farm | $1,817 |

| Altamont | $3,850 | State Farm | $1,671 |

| Alton | $4,634 | State Farm | $1,663 |

| Altoona | $3,880 | State Farm | $1,713 |

| Americus | $3,702 | State Farm | $1,700 |

| Andale | $4,839 | State Farm | $1,891 |

| Andover | $4,571 | State Farm | $1,825 |

| Anthony | $4,506 | State Farm | $2,056 |

| Arcadia | $3,731 | State Farm | $1,663 |

| Argonia | $4,619 | State Farm | $2,013 |

| Arkansas City | $4,566 | State Farm | $1,863 |

| Arlington | $4,578 | State Farm | $1,954 |

| Arma | $3,712 | State Farm | $1,644 |

| Arnold | $4,950 | State Farm | $2,081 |

| Ashland | $4,905 | State Farm | $2,058 |

| Assaria | $4,344 | State Farm | $1,777 |

| Atchison | $3,289 | State Farm | $1,573 |

| Athol | $4,688 | State Farm | $1,855 |

| Atlanta | $4,517 | State Farm | $1,663 |

| Attica | $4,538 | State Farm | $1,987 |

| Atwood | $4,556 | State Farm | $1,643 |

| Auburn | $3,627 | State Farm | $1,634 |

| Augusta | $4,580 | State Farm | $1,852 |

| Aurora | $3,890 | State Farm | $1,663 |

| Axtell | $3,636 | State Farm | $1,767 |

| Baileyville | $3,599 | State Farm | $1,663 |

| Baldwin City | $3,140 | State Farm | $1,600 |

| Barnard | $4,280 | State Farm | $1,663 |

| Barnes | $3,743 | State Farm | $1,767 |

| Bartlett | $3,770 | State Farm | $1,663 |

| Basehor | $3,272 | State Farm | $1,529 |

| Baxter Springs | $3,803 | State Farm | $1,685 |

| Bazine | $5,042 | State Farm | $2,054 |

| Beattie | $3,698 | State Farm | $1,756 |

| Beaumont | $4,311 | State Farm | $1,663 |

| Beeler | $4,961 | State Farm | $1,663 |

| Bel Aire | $4,836 | State Farm | $1,816 |

| Belle Plaine | $4,665 | State Farm | $1,895 |

| Belleville | $3,792 | State Farm | $1,720 |

| Beloit | $3,917 | State Farm | $1,719 |

| Belpre | $4,810 | State Farm | $1,663 |

Rates are for a policy with $350,000 of dwelling coverage.

What kind of home insurance do I need in Kansas?

Kansas being in the plains means its weather can change frequently and dramatically. Strong storms are common, and it's important to make sure that your home insurance covers you.

Does Kansas home insurance cover wind and tornadoes?

Home insurance almost always includes coverage for wind and tornado damage. It never hurts to check, though, especially because of how common wind damage is in Kansas. The state experienced 45 tornadoes and 666 nontornado windstorms in 2025, according to the NOAA/National Weather Service Storm Prediction Center.

Home insurance policies often include a separate deductible for wind and hail damage. For example, you might pay a $1,000 deductible if you file a claim for water damage. But if you file a claim for wind or hail damage, you could pay a higher amount. Make sure you know if your policy has a wind and hail deductible and how much it is, so you're prepared if you need to file a claim.

Does home insurance in Kansas cover hail damage?

Home insurance usually covers hail damage. That's good news, considering that hail is very common in the state. Kansas had 375 hailstorms in 2025, according to the NOAA/National Weather Service Storm Prediction Center.

Your policy might have a separate wind and hail deductible, similar to tornado damage. And if your roof or other parts of your home are old or not well-maintained, you might not have any coverage.

Does Kansas home insurance cover floods?

Regular home insurance does not cover flood damage. You need to buy a separate flood insurance policy to get flood coverage. You can get a policy from the National Flood Insurance Program (NFIP) or directly from some insurance companies.

Since 2015, the NFIP has paid out over $28 million in damage for 845 flood claims in Kansas.

How to save on Kansas home insurance

Home insurance in Kansas isn't usually cheap, but you can work to lower your rate in a few ways.

Each home insurance company sets its own rates. That means comparing quotes can help you find the cheapest price for the coverage you need. You can do this yourself by getting several quotes online, by phone or in person. Or you can have an independent agent get quotes for you. | |

Bundling just means insuring your home and cars with the same company. Bundling discounts are some of the biggest savings that companies offer. You might also get a bundling discount for buying umbrella, boat or motorcycle insurance. | |

Roof damage is common in Kansas and is usually caused by wind or hail. Newer roofs are less likely to be damaged, so you'll often get a discount. If you don't want to get a new roof, keeping yours in good condition can lower the risk of damage. This helps keep your rates low because you're less likely to file a claim. |

Having a realistic expectation of cost is important, and Kansas home insurance is expensive. Buying a policy just because it has a cheap rate could mean you're missing important coverage. That can cost you more in the long run, since you would have to pay for more home repairs yourself.

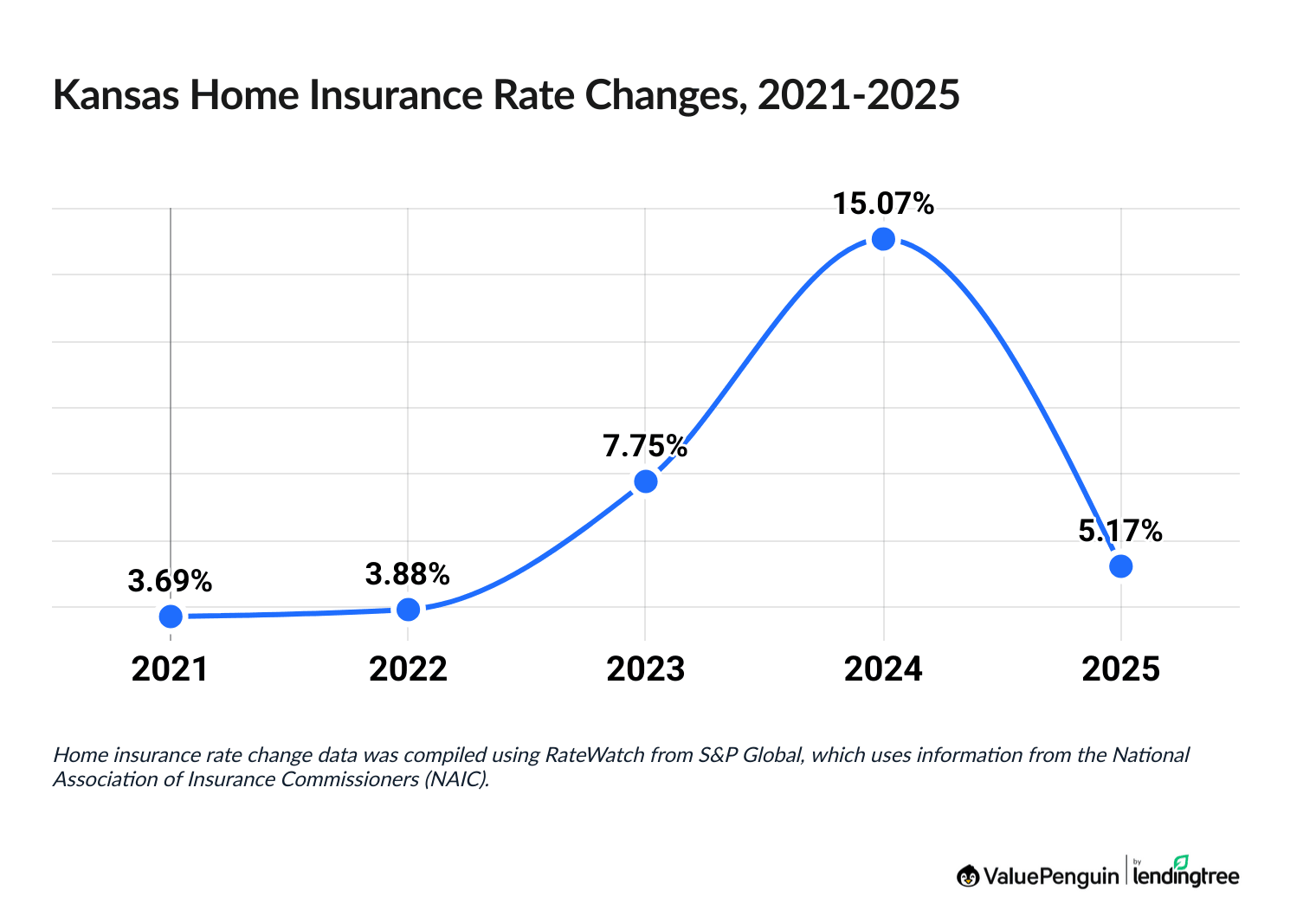

Are home insurance rates going up in Kansas?

Home insurance prices have gone up about 42% in Kansas over the last five years.

But rate increases seem to be slowing down. Rates went up by 5.17% in 2025, much lower than the peak increase of 15.07% in 2024.

Home insurance rate increases in Kansas, 2021-2025

Year | Avg. rate increase |

|---|---|

| 2021 | 3.69% |

| 2022 | 3.88% |

| 2023 | 7.75% |

| 2024 | 15.07% |

| 2025 | 5.17% |

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Liberty Mutual raised rates the most, with the cost of policies going up about 81% over the last five years. Shelter had the lowest rate increase over this period, at 11%.

Frequently asked questions

How much is home insurance in Kansas?

Home insurance costs an average of $4,095 per year in Kansas. That's 71% more per year than the national average, which is $2,395. It's the fourth-most-expensive state for home insurance, behind Oklahoma, Nebraska and Colorado.

Who has the cheapest homeowners insurance in Kansas?

State Farm has the cheapest home insurance in Kansas for most people, with an average rate of $1,732 per year for a policy with $350,000 in dwelling coverage. Shelter and Farmers also tend to be cheap options.

Why is Kansas home insurance so expensive?

Kansas home insurance is expensive because the risk for home damage, usually from tornadoes and wind, is high. The more likely homes are to be damaged, the higher the insurance rates will be. That's because insurance companies know they'll have to pay claims, so they charge higher rates to prepare.

Methodology

To find the best and cheapest home insurance in Kansas, ValuePenguin's experts got home insurance quotes from eight of the top insurance companies in every residential ZIP code in the state. The quotes are for a 45-year-old married man with no home insurance claims. The house used for the quotes is 2,020 square feet and was built 48 years ago. This is representative of the average home in Kansas.

Our experts used the following coverage limits to get average rates for a variety of home values:

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

All rates are from Quadrant Information Services, which gets rates from publicly available insurance company filings. Home insurance costs change based on your age, location, home info, claims and more. Your quotes will likely be different from the quotes in this report.

Ratings for each insurance company are based on ValuePenguin's analysis of average rates, coverages, discounts, customer complaint data from the National Association of Insurance Commissioners (NAIC) and scores from J.D. Power's home insurance customer satisfaction survey.

Sources:

About the Author

Senior Writer

Cate Deventer is a Senior Writer who specializes in health insurance, Medicare, auto and home insurance. She's been a licensed insurance agent since 2011.

She started her insurance career working as a customer service agent for State Farm. She later moved to an independent agency, where she worked with several insurance companies and hundreds of clients. She quoted policies, filed claims and answered insurance questions. In 2021, she pivoted her career and began writing about insurance for Bankrate. She moved to ValuePenguin in 2023 and began writing about health insurance and Medicare.

Cate has a passion for helping readers choose insurance to fit their needs. She enjoys knowing that her research and knowledge help people choose insurance products that make a positive difference in their lives.

How insurance helped Cate

Cate used her health insurance knowledge to navigate a surgery in 2023. Understanding how her policy worked let her focus on recovery instead of worrying about bills.

Expertise

- Health insurance

- Medicare & Medicaid

- Auto insurance

- Home insurance

- Life insurance

Credentials

- Licensed Life, Accident & Health Insurance Agent

- Licensed Property & Casualty Insurance Agent

Referenced by

- CBS

- NBC

- Wall Street Journal

Education

- BA, Theatre, Purdue University

- BA, English, Indiana University

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.