Best Cheap Health Insurance in Idaho (2026)

Select Health has the best health insurance in Idaho. Silver plans from Select Health start at $482 per month before discounts.

Find Cheap Health Insurance Quotes in Idaho

Best and cheapest health insurance in Idaho

Cheapest health insurance companies in Idaho

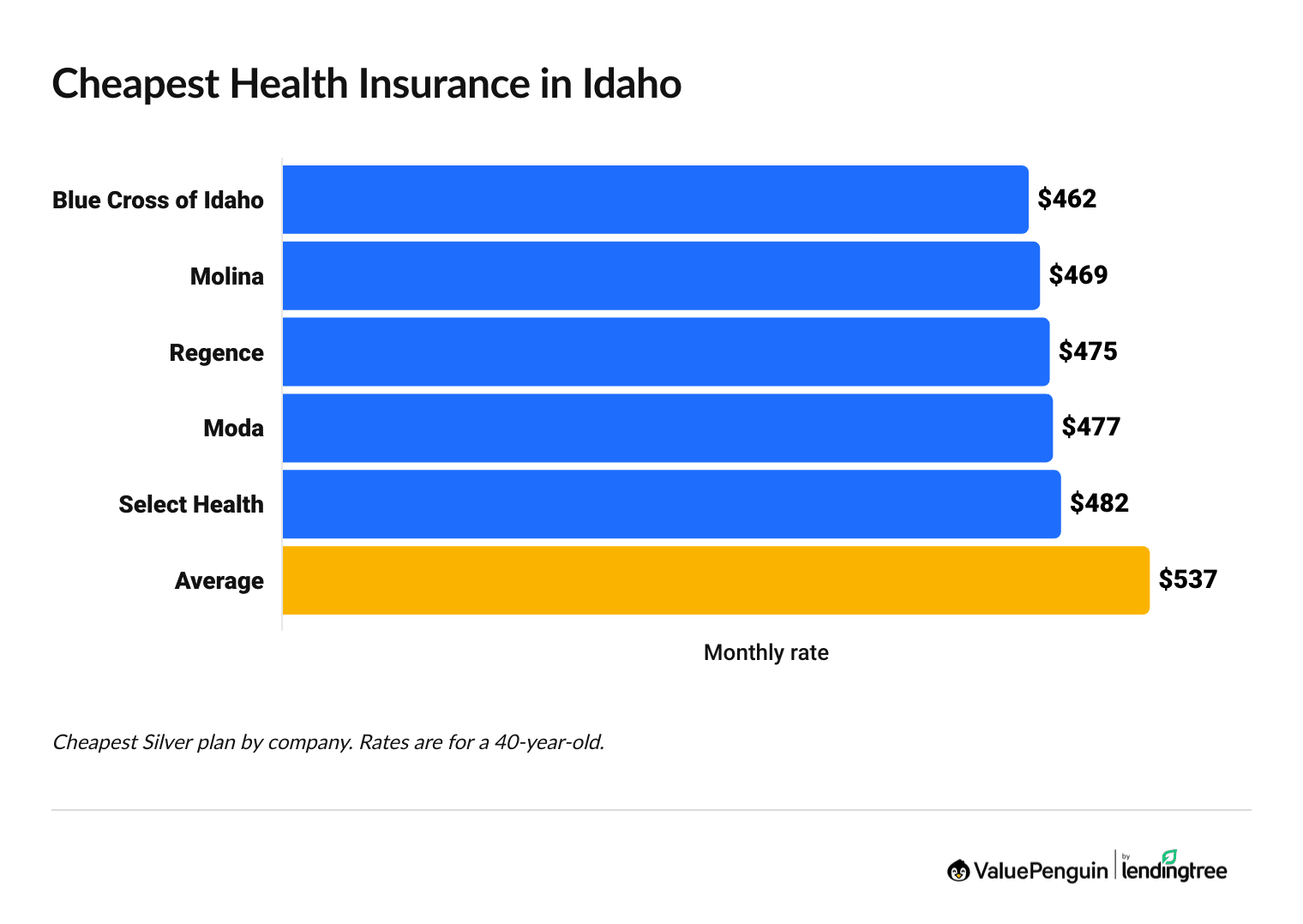

Blue Cross of Idaho, Molina and Regence Blue Shield of Idaho sell the cheapest health insurance plans in ID, with Silver rates starting at $462 per month before discounts.

Find Cheap Health Insurance Quotes in Idaho

Affordable health insurance in Idaho

Company |

ACA rating

|

VP rating

|

|---|---|---|

| Blue Cross of Idaho | $462-$564 | |

| Molina Healthcare of Idaho | $469-$568 | |

| Regence BlueShield of Idaho | $475-$584 | |

| Moda Health | $477-$589 | |

| Select Health | $482-$639 | |

| Mountain Health CO-OP | $491-$643 | |

| St. Luke's Health Plan | $509-$559 | |

| PacificSource Health Plans | $536-$655 |

- Blue Cross of Idaho sells the cheapest Silver plans in Idaho, with rates as low as $462 per month. Blue Cross is also the second-most-popular company in Idaho, selling more than a quarter of all health insurance plans in the state.

- Bronze plans give you cheaper rates than Silver plans but require you to pay more toward your medical bills. For most people, a Silver plan is a better option. But if you want a Bronze plan, Moda is the cheapest for most people.

- In some of the state's largest cities, Moda is the cheapest company. Moda has the cheapest rates in Boise, Meridian, Nampa and Caldwell.

Cheapest Bronze plans in Idaho: Moda

If you want a Bronze plan to get cheaper rates, Moda is a good option.

Moda's Bronze plans start at $326 per month before discounts. Roughly 90% of Idaho's population can get a cheap Bronze plan from Moda.

Bronze is the most popular plan level in Idaho, but this coverage has major drawbacks. Bronze plans have the cheapest monthly rates, but you'll have to pay more when you go to the doctor or fill a prescription.

Bronze plans usually only make sense if you're young, mostly healthy and you don't need much medical care. If you get a Bronze plan, make sure to have savings in the bank to pay for the higher share of your medical bills.

Best health insurance companies in Idaho

Select Health has the best health insurance plans in Idaho.

Select Health has a high 4-star rating, the highest in the state, from HealthCare.gov. It gets a perfect 5-star rating for customer experience.

Find Cheap Health Insurance Quotes in Idaho

Best-rated health insurance companies in Idaho

Company |

ACA rating

|

VP rating

|

|---|---|---|

| Select Health | 4.0 out of 5 | 4.0 out of 5 |

| St. Luke's Health Plan | 4.0 out of 5 | 4.0 out of 5 |

| Blue Cross of Idaho | 3.0 out of 5 | 4.0 out of 5 |

| Mountain Health CO-OP | 3.0 out of 5 | 4.0 out of 5 |

| Regence BlueShield of Idaho | 3.0 out of 5 | 4.0 out of 5 |

| Moda Health | 3.0 out of 5 | 4.0 out of 5 |

| Molina Healthcare of Idaho | N/A | 4.0 out of 5 |

| PacificSource Health Plans | 3.0 out of 5 | 3.5 out of 5 |

Blue Cross of Idaho also has excellent customer service and wide availability across the state. One hundred percent of Idaho's population can get a Blue Cross plan.

How much does health insurance cost in Idaho?

The average cost of health insurance in Idaho is $537 per month, but you could pay $252 per month, on average, if you get discounts based on your income.

Find Cheap Health Insurance Quotes in Idaho

- Your rate changes based on your age and what plan tier you buy. It also depends on the number of people you insure on your plan, the company you choose, whether or not you use tobacco and where you live in Idaho.

- Bronze plans usually have the cheapest monthly rates. That's because they cover the lowest amount of your medical bills. Higher-tier plans, like Gold and Platinum, cost more because they pay for more of your medical bills.

Health insurance discount changes in Idaho for 2026

Health insurance costs $252 per month on average in Idaho, if you get discounts based on your income.

For people who can get subsidies, rates will increase from about $139 That's because discount levels are changing for 2026. Since 2021, shoppers on HealthCare.gov and state marketplaces have gotten larger discounts called "expanded subsidies." These better discounts expire at the end of 2025. While you may still be able to get discounts based on your income, they likely won't be as good as they were before.

Health insurance rates in Idaho after subsidies (2025 vs. 2026)

Income | 2025 rate | 2026 rate | Difference |

|---|---|---|---|

$30,000 | $49 | $155 | 216% |

| $40,000 | $154 | $287 | 86% |

| $50,000 | $283 | $415 | 47% |

| $60,000 | $423 | $490 | 16% |

| $70,000+ | $436 | $490 | 12% |

Average cost after subsidies for a single 40-year-old with a Benchmark Silver plan.

- What they are: You can get discounts on your monthly rate if you have a low income. The discounts are called subsidies or tax credits.

- How to qualify: If you're single, you have to make between $15,650 and $62,600 per year to get subsidies. For a family of four, the range is $32,150 and $128,600 per year. The lower your income, the bigger your discount. If you can get Medicaid, you can't get subsidies.

- How to use them: You can use a subsidy to lower the rate of any Bronze, Silver, Gold or Platinum plan (but not Catastrophic plans) from any health insurance company in Idaho. You have to shop on Your Health Idaho to get the discounts. How much do you save? You can use ValuePenguin's subsidy calculator to find out how much a subsidy will lower your health insurance rate.

Cheap Idaho health insurance plans by city

Moda sells the cheapest health insurance in Boise, Idaho.

Moda also has the cheapest Silver plans in Meridian, Nampa and Caldwell. But Blue Cross of Idaho, Molina, Mountain Health CO-OP and Regence also have cheap rates, depending on where you live. For example, Molina is cheapest in Coeur d'Alene and Post Falls, while Regence BlueShield of Idaho is cheapest in Pocatello.

Cheapest health insurance plans by ID county

County | Cheapest plan | Monthly rates |

|---|---|---|

| Ada | Moda Select Idaho Silver | $477 |

| Adams | Moda Select Idaho Silver | $477 |

| Bannock | Regence ICON Silver | $475 |

| Bear Lake | Regence ICON Silver | $475 |

| Benewah | Regence ICON Silver | $479 |

| Bingham | Regence ICON Silver | $475 |

| Blaine | Mountain Health CO-OP LINK SILVER | $504 |

| Boise | Moda Select Idaho Silver | $477 |

| Bonner | Molina Silver Saver | $479 |

| Bonneville | Molina Silver Saver | $469 |

| Boundary | Regence ICON Silver | $479 |

| Butte | Blue Cross East Silver | $488 |

| Camas | Mountain Health CO-OP LINK SILVER | $504 |

| Canyon | Moda Idaho Silver | $477 |

| Caribou | Regence ICON Silver | $475 |

| Cassia | Mountain Health CO-OP LINK SILVER | $504 |

| Clark | Blue Cross East Silver | $488 |

| Clearwater | Blue Cross North Central Silver | $462 |

| Custer | Blue Cross East Silver | $488 |

| Elmore | Moda Select Idaho Silver | $477 |

| Franklin | Regence ICON Silver | $475 |

| Fremont | Blue Cross East Silver | $488 |

| Gem | Moda Select Idaho Silver | $477 |

| Gooding | Mountain Health CO-OP LINK SILVER | $504 |

| Idaho | Blue Cross North Central Silver | $462 |

| Jefferson | Blue Cross East Silver | $488 |

| Jerome | Mountain Health CO-OP LINK SILVER | $504 |

| Kootenai | Molina Silver Saver | $479 |

| Latah | Blue Cross North Central Silver | $462 |

| Lemhi | Blue Cross East Silver Connect | $488 |

| Lewis | Blue Cross North Central Silver | $462 |

| Lincoln | Mountain Health CO-OP LINK SILVER | $504 |

| Madison | Blue Cross East Silver | $488 |

| Minidoka | Mountain Health CO-OP LINK SILVER | $504 |

| Nez Perce | Blue Cross North Central Silver | $462 |

| Oneida | Regence ICON Silver | $475 |

| Owyhee | Moda Select Idaho Silver | $477 |

| Payette | Moda Select Idaho Silver | $477 |

| Power | Regence ICON Silver | $475 |

| Shoshone | Regence ICON Silver | $479 |

| Teton | Blue Cross East Silver | $488 |

| Twin Falls | Mountain Health CO-OP LINK SILVER | $504 |

| Valley | Mountain Health CO-OP LINK SILVER | $491 |

| Washington | Moda Select Idaho Silver | $477 |

Cheapest Silver plan with rates for a 40-year-old

Find Cheap Health Insurance Quotes in Idaho

Best health insurance by level of coverage

The best health insurance for you depends on how much medical care you need, your monthly budget and the plans available where you live.

To choose a health insurance plan, start by thinking about how often you go to a doctor and how expensive your treatments are. If you go to the doctor often, a Gold or Platinum plan might be the best choice. But if you're healthy and you don't need much health care, a Silver or Bronze plan could be better.

Platinum plans: Best if you have high medical costs

| Platinum plans pay for about 90% of your medical care. |

Platinum plans cost $649 per month, on average, in Idaho.

Platinum health insurance plans have the highest monthly rates in Idaho. But these plans can be a good idea if you have a lot of medical costs because they let you pay less when you get care. Platinum plans have the lowest deductibles, coinsurance and copays.

Overall, the most you could spend on medical care, called the out-of-pocket maximum, is the lowest with Platinum plans.

Gold plans: Best if you need frequent medical care

| Gold plans pay for about 80% of your medical care. |

In Idaho, Gold plans cost $569 per month, on average.

Gold plans also pay for a large portion of your medical bills. But they're a bit cheaper than Platinum plans. If you need frequent medical care or think you might have expensive medical bills in the coming year, a Gold plan might be a good idea.

Silver plans: Best for most people

| Silver plans pay for about 70% of your medical care. |

Silver plans cost an average of $537 per month in Idaho.

Silver plans are a good option if you have average medical needs. They're a middle-ground option that balances moderate rates with good coverage. Plus, if you have a low income, you might get extra discounts called cost-sharing reductions that make your medical bills cheaper.

Bronze plans: Best if you're mostly healthy

| Bronze plans pay for about 60% of your medical care. |

Bronze plans cost $395 per month, on average, in Idaho.

Bronze plans have low rates because they make you pay more when you go to the doctor. Because you'll pay a higher share of your medical bills, you should take a close look at your finances before buying a Bronze plan. Make sure you can afford to pay the higher costs if something serious happens. You could pay more than $8,200 per year toward your medical bills if you buy a Bronze plan.

Even though they're not the best option for most people, Bronze plans are the most popular plan tier in Idaho. About half of everyone who buys a plan on Your Health Idaho buys a Bronze plan.

Like other plan levels, Bronze covers preventive care for free. Some Bronze plans also cover things like generic prescriptions or urgent care visits for free or a reduced fee before you meet the deductible. When you shop for a Bronze plan, look at the benefits of the plan before the deductible is met. This could help you get the best coverage.

Catastrophic plans: Best as a last resort

Catastrophic plans cost an average of $221 per month for a 21-year-old.

These plans are only a good idea if you can't afford anything else and you can't get Medicaid. You have to pay a very large share of your medical bills with a Catastrophic plan, and you also can't use subsidies to make the monthly rate cheaper. Catastrophic plans are better than not having any health insurance, but you'll be better off with a Bronze or Silver plan, especially if you qualify for rate discounts.

You can only get a Catastrophic plan if you're under 30 or you qualify for an exemption. This essentially means that something happened to prevent you from getting better health insurance. For example, you might qualify for a financial or hardship exemption if you can't afford any other type of health insurance, were homeless, got evicted or experienced a natural disaster.

Cheap or free health insurance in Idaho if you have a low income

You might be able to get free health insurance through Idaho's Medicaid program if you have a low income. If you can't get Medicaid, buying a Silver plan could be a good idea because you can potentially get low-income discounts.

Medicaid in Idaho

Medicaid is cheap or free health insurance from the government. You might qualify if you make less than $22,000 per year if you're single or $44,000 per year if you're part of a family of four.

Although Medicaid is mostly for people with low incomes, you might also qualify if you have a disability, are blind or are a woman with breast or cervical cancer.

Use cost-sharing reductions for cheaper medical care

If you have a low income, a Silver plan might also be a good option. If you make between $15,650 and $39,125 per year as an individual or between $32,150 and $80,375 per year as a family of four, you can get discounts called cost-sharing reductions (CSRs). These discounts lower your plan's deductible, copay, coinsurance and out-of-pocket maximum costs, so you pay for less of your health care. You can only get CSRs on Silver plans.

If you qualify for cost-sharing reductions, you can probably also get subsidies that make your monthly rate cheaper. But keep in mind that if you can get Medicaid, you can't get rate subsidies or cost-sharing reductions.

Are health insurance rates going up in ID in 2026?

Overall, health insurance rates in Idaho went up by an average of 11% between 2025 and 2026.

Bronze plans, the most popular plan level in the state, went up by 9% more in 2026 than in 2025. But Platinum plans went up by 16% for 2026. Silver and Gold plans went up by about 10%. Silver plans have gone up by 4% in the last five years.

Bronze

Silver

Gold

Platinum

Year | Cost | Change |

|---|---|---|

| 2022 | $368 | – |

| 2023 | $353 | -4% |

| 2024 | $347 | -2% |

| 2025 | $363 | 4% |

| 2026 | $395 | 9% |

Monthly costs are for a 40-year-old. Expanded Bronze plans are included in 2024, 2025 and 2026 averages, when they're offered.

Why is health insurance expensive in Idaho in 2026?

Health care costs keep going up, which in turn makes health insurance more expensive.

That's because health insurance companies have to pay more when it gets more expensive for you to go to the doctor or get medications. To make up for the added costs, medical insurance companies raise rates for everyone. In Idaho, health insurance companies have increased rates by 11% on average.

One of the main reasons health insurance rates are going up has to do with the cost for weight-loss drugs, such as Ozempic and Wegovy. These medications are expensive and becoming widely used, which means they cost health insurance companies a lot of money. To balance the high costs, companies raise rates across the board.

However, rates for weight-loss medications are expected to go down in 2026, which could have a positive impact on rates for 2027.

Another reason costs are higher in 2026 is because of a possible change to discounts. Since 2021, people with low incomes have gotten bigger discounts called "enhanced subsidies." However, these extra savings expire at the end of 2025 unless Congress renews them. That means the discounts on the marketplace in 2026 will be smaller. They'll still save you money if you qualify, just not as much.

How to prepare for the 2026 rate increases

- Get quotes and shop around. If your plan's rates go up in 2026, look at the other companies and plans in your area and see if there's a cheaper option. Just make sure your doctors take the plan before you commit to it.

- See if you can get discounts. Even though the discounts next year might not be as big as they are now, they can still save you money if you qualify. You can use a subsidy calculator to see if you can get discounts.

- Consider a lower-tier plan. A lower-tier plan, such as Bronze, can be a good idea if you need a cheaper monthly rate. However, you have to pay for more of your medical bills yourself with a Bronze plan. To help you save, consider opening a health savings account (HSA). In 2026, Bronze plans are considered high-deductible health plans, which means you can get an HSA when you sign up.

- Check if you can get Medicaid. You can get Medicaid in Idaho if you make less than about $22,000 per year as an individual. Medicaid can make your health care free or very cheap.

Idaho's health insurance rates have stayed steady partly because of the state's "Reinsurance Waiver." Usually, health insurance companies pay claims for everyone, including people with expensive health needs. But with Idaho's Reinsurance Waiver, money is set aside in a separate program to pay the claims for people with expensive medical needs. This helps companies keep rates lower. And nothing changes for shoppers; they still have medical insurance through the company of their choosing. Everything happens behind the scenes, and your coverage works like normal.

To get health insurance in Idaho, you can shop on Your Health Idaho between Oct. 15 and Dec. 16 every year. You might be able to get a plan outside this window if you've moved, gotten married, had a baby or experienced another qualifying life change.

COBRA insurance in Idaho

COBRA costs an average of $718 per month in Idaho.

It's almost always cheaper to get a plan from Your Health Idaho, the state's medical insurance marketplace, than to get COBRA insurance. A plan from Your Health Idaho costs $537 per month, on average. Even a Platinum plan, which covers the largest share of your medical bills of any plan tier, costs $649 per month, on average. That's still more than $69 per month cheaper than COBRA.

COBRA insurance lets you keep the health insurance plan you had at a job when you leave, are fired or retire. Usually, coverage lasts up to a year and a half, but it can sometimes last up to three years.

But your employer won't chip in to pay part of the monthly rate anymore. You have to pay the full cost for a plan, which is why COBRA tends to be expensive.

Short-term health insurance in Idaho

At the start of 2025, the administration rolled back a rule that would have limited short-term health plans to three months. Although the administration hasn't said when this change will happen, sometime in the coming year, you may be able to get short-term health insurance plan in Idaho that last up to 364 days and can be renewed for up to three years total.

If you only need coverage for a short period of time, you can buy short-term health insurance in Idaho. But plans aren't available on the state's health insurance marketplace. You have to buy coverage directly from a short-term health insurance company.

Pros of short-term health insurance in Idaho

Cons of short-term health insurance in Idaho

In Idaho, you can buy "enhanced" short-term plans. These plans are similar to marketplace coverage because they have to offer the same level of coverage. Companies also aren't allowed to consider your health history when setting rates or approving coverage.

Health insurance enrollment by income level in Idaho

Health insurance discounts getting smaller in 2026 impacts people with low incomes the most.

People with lower incomes are more likely to get health insurance from the Your Health Idaho marketplace than they are to get a plan from their employer. In Idaho in 2025, more than half of people with a marketplace plan made less than $37,650.

Income | % of total enrollment |

|---|---|

| Less than $15,060 | 2% |

| $15,060 to $20,783 | 3% |

| $20,784 to $22,590 | 6% |

| $22,591 to $30,120 | 24% |

| $30,121 to $37,650 | 21% |

| $37,651 to $45,180 | 14% |

| $45,181 to $60,240 | 13% |

| $60,241 to $75,300 | 5% |

| $75,301 or more | 4% |

| Other/unknown | 10% |

Enrollment in 2025 marketplace plans made during the 2024-2025 Open Enrollment period. Total may not be 100% due to rounding

Frequently asked questions

How much does health insurance cost per month in Idaho?

Health insurance in Idaho costs an average of $537 per month for a Silver plan. But your rate may be lower if you get discounts based on your income. Your rate depends on the company you pick, your age, the plan tier you buy, where you live, how many people you want the plan to cover and whether or not you smoke or use tobacco.

Does Idaho have Affordable Care Act insurance?

Yes. You can buy Affordable Care Act plans, also called "Obamacare" plans, from Idaho's state marketplace, Your Health Idaho.

Who can buy health insurance from Your Health Idaho?

You must be a U.S. citizen, national or lawfully present in the United States for the entire time that you have health insurance. You also need to live in Idaho and be a resident of the United States.

When can I buy health insurance in Idaho?

Open enrollment in Idaho starts on Oct. 15 and ends Dec. 16. That's earlier than in most states, which let you buy medical insurance between Nov. 1 and Jan 15. If you've recently moved, gotten married, had a child or otherwise qualified for a special enrollment period, you can buy health insurance outside of the open enrollment time frame.

Is $500 a month normal for health insurance in Idaho?

Yes, $500 per month is roughly average for health insurance in Idaho, depending on your age and the plan level you buy. On average, a 40-year-old pays $537 per month for a Silver plan before discounts, while a 21-year-old pays $413 for the same coverage. But you could get a cheaper rate if you have a low income and you get discounts.

Who qualifies for subsidies for Idaho health insurance?

You may qualify for health insurance subsidies in Idaho if your income level falls below a certain limit. For single people, you may qualify if you make between $15,650 and $62,600. Couples may qualify if they make between $21,150 and $84,600 combined. Families of four may qualify if they make between $32,150 and $128,600.

Methodology and sources

Idaho health insurance rate data for 2026 is from Idaho's state exchange, Your Health Idaho. ValuePenguin used the marketplace data to find average rates for different plan tiers, geographic locations and family sizes.

Rates

Rates are based on a 40-year-old with a Silver plan, unless otherwise noted. Rates for Bronze plans include regular and Expanded Bronze plans for 2024, 2025 and 2026, when the plans are available. Your costs and plan options will vary; plans aren't always available in all parts of a state or county.

Subsidies

Rates after subsidies are estimates for a 40-year-old with a Benchmark Silver plan and are based on how subsidies were structured before 2021. Prices are calculated using KFF's rates for full-price Benchmark plans, federal poverty levels (FPLs), IRS rules about premium tax credits and Congressional reports about expanded tax credits. The total cost in the state uses calculated rates by income, which are weighted using CMS data on the incomes of those who purchased plans during last year's open enrollment. The median was used for each income range. Unknown incomes were excluded from the calculations. Incomes of 100% of the federal poverty level and 500% of the federal poverty level were assumed for enrollees who earn less than 100% FPL and more than 500% FPL, respectively. Information about state subsidies, when available, was sourced from state marketplaces.

Ratings

ValuePenguin's experts rank companies based on cost, coverage options, customer satisfaction and unique value. Ratings are out of 100 possible points. ACA ratings show how the company performs in Idaho for medical care, member experience and plan administration. This 2026 plan quality data from CMS is based on data from last year. Ratings are not available for new plans or plans with low enrollment.

More sources

Enrollment trends, including plan selections by tier and enrollment by income, are from CMS data for the 2025 open enrollment period.

Info about rate increase requests from Idaho insurance companies comes from the Peterson-KFF Health System Tracker.

Other sources include S&P Global Capital IQ and the National Association of Insurance Commissioners (NAIC). Data about GLP-1 medication price changes for 2026 are from CNBC.

About the Author

Senior Writer

Cate Deventer is a Senior Writer who specializes in health insurance, Medicare, auto and home insurance. She's been a licensed insurance agent since 2011.

She started her insurance career working as a customer service agent for State Farm. She later moved to an independent agency, where she worked with several insurance companies and hundreds of clients. She quoted policies, filed claims and answered insurance questions. In 2021, she pivoted her career and began writing about insurance for Bankrate. She moved to ValuePenguin in 2023 and began writing about health insurance and Medicare.

Cate has a passion for helping readers choose insurance to fit their needs. She enjoys knowing that her research and knowledge help people choose insurance products that make a positive difference in their lives.

How insurance helped Cate

Cate used her health insurance knowledge to navigate a surgery in 2023. Understanding how her policy worked let her focus on recovery instead of worrying about bills.

Expertise

- Health insurance

- Medicare & Medicaid

- Auto insurance

- Home insurance

- Life insurance

Credentials

- Licensed Life, Accident & Health Insurance Agent

- Licensed Property & Casualty Insurance Agent

Referenced by

- CBS

- NBC

- Wall Street Journal

Education

- BA, Theatre, Purdue University

- BA, English, Indiana University

Editorial note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.